.svg)

Six Proposed Hospital Mergers–And How They Would Affect Hospital Concentration in Their Communities

.webp)

A new tool from the Health Care Affordability Lab at Yale allows users to explore how hospital mergers, closures, ownership changes, and rising market concentration are reshaping U.S. hospital markets and potentially driving up prices. State and local policymakers may find this tool especially useful as they look for ways to bring down health care costs or prevent further increases.

The tool’s Forecast Lab feature allows users to simulate hospital ownership changes and forecast the impact of those changes on a hospital market’s concentration, as measured by the Herfindahl–Hirschman Index (HHI)—a standard antitrust metric used to measure market concentration. HHIs range from 0 (many small competitors, unconcentrated) to 10,000 (a monopoly). Mergers that produce a post-merger HHI above 1,800 via an increase of more than 100 points are considered Red Zone Mergers and, according to the Department of Justice and Federal Trade Commission guidelines, are likely to raise prices by lessening competition.

Not all mergers or transactions are problematic. Our researchers used the Forecast Lab feature of the tool to analyze the impact of several proposed mergers—from Indiana to Washington state to West Virginia. They found that two proposed mergers would increase market concentration in one or more hospital markets, one would decrease concentration, and three would not impact concentration.

These analyses are based on calculations made with the best available data, which we verify using press releases, news stories, and hospital systems’ financial reporting documents. However, the data may be incomplete, particularly regarding changes to hospital ownership that occurred after 2023, a period for which we rely exclusively on these verification methods.

In order to measure concentration, we define markets based on a 30-minute travel time. This definition reflects our best effort to approximate a reasonable choice set for patients and does not necessarily represent the relevant market for antitrust enforcement.

Proposed Mergers That Would Increase Concentration

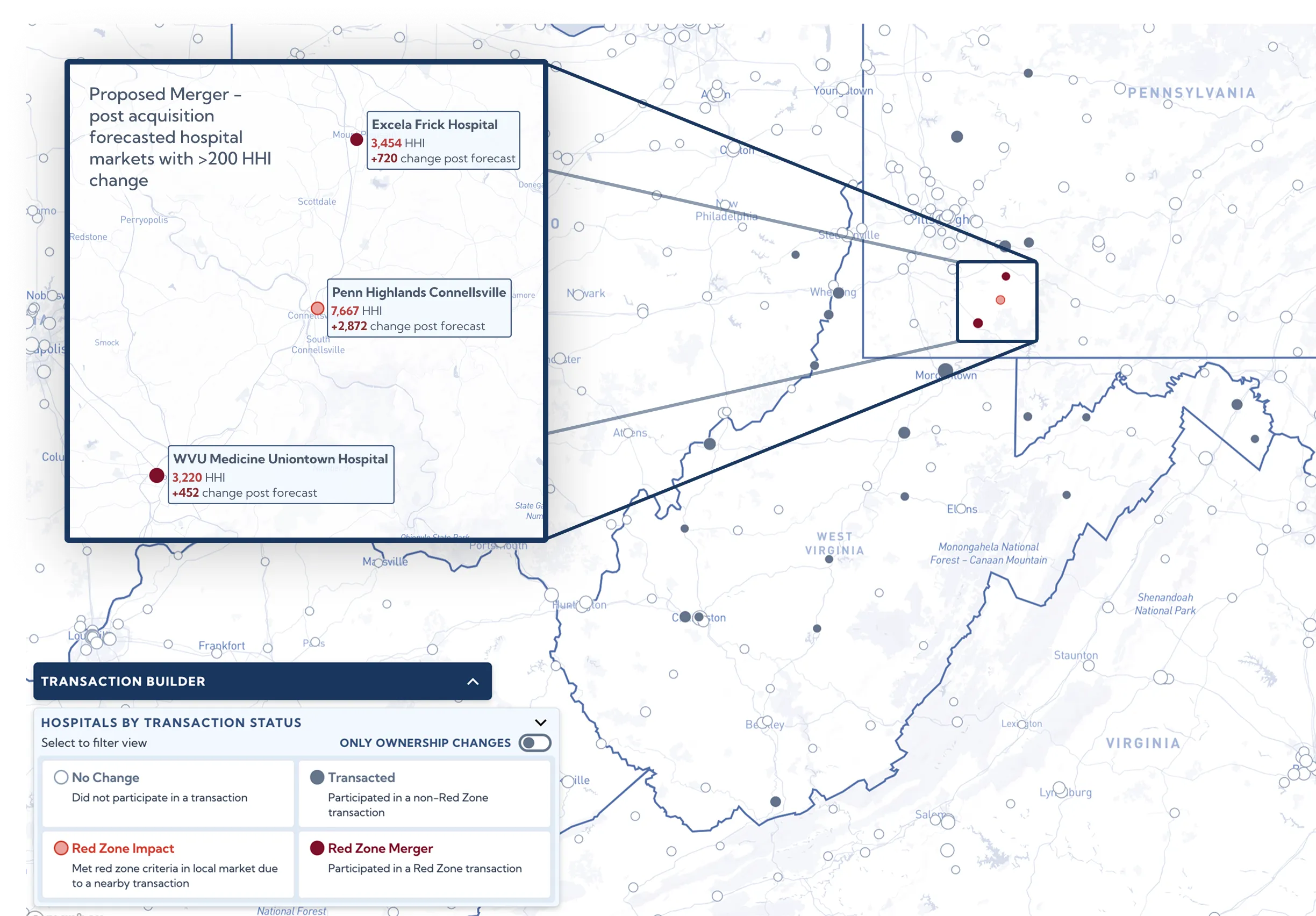

WVU Health System (Morgantown, WV) acquiring Independence Health System (Greensburg, PA).

West Virginia-based WVU Health System1 is seeking to acquire Pennsylvania-based Independence Health System’s five hospitals. The transaction is expected to close in fall 2026.

Forecasted Impact: This is a RED ZONE MERGER, and it would increase the HHI of three hospitals in Pennsylvania, all in markets with “high” (1,800 to <5,000 HHI) or “higher” (5,000 to <10,000 HHI) concentration.

| Classification | Red Zone Merger |

| Combined System Size | 30 hospitals |

| Markets with Increased Concentration | 3 (2 merging + 1 nearby) |

| Largest HHI Increase | +2,872 (Penn Highlands Connellsville) |

Key Facts:

- This merger would increase Excela Frick Hospital’s (Mount Pleasant, PA) HHI by 720, resulting in a post-merger HHI of 3,454, further increasing concentration in an already “high” concentration market.

- This merger would give WVU two additional hospitals in “high” concentration markets (1,800 to <5,000 HHI) and three additional hospitals in “higher” concentration markets (5,000 to <10,000). According to our dataset, WVU has eight hospitals in monopoly markets, 10 hospitals in “higher” concentration markets, and two hospitals in “high” concentration markets.

- Outside of the hospitals WVU currently owns and those it is seeking to acquire, the merger would increase concentration in the Penn Highlands Connellsville (Connellsville, PA) market by 2,872 HHI points, resulting in an HHI of 7,667 and moving the market from the “high” to “higher” category.

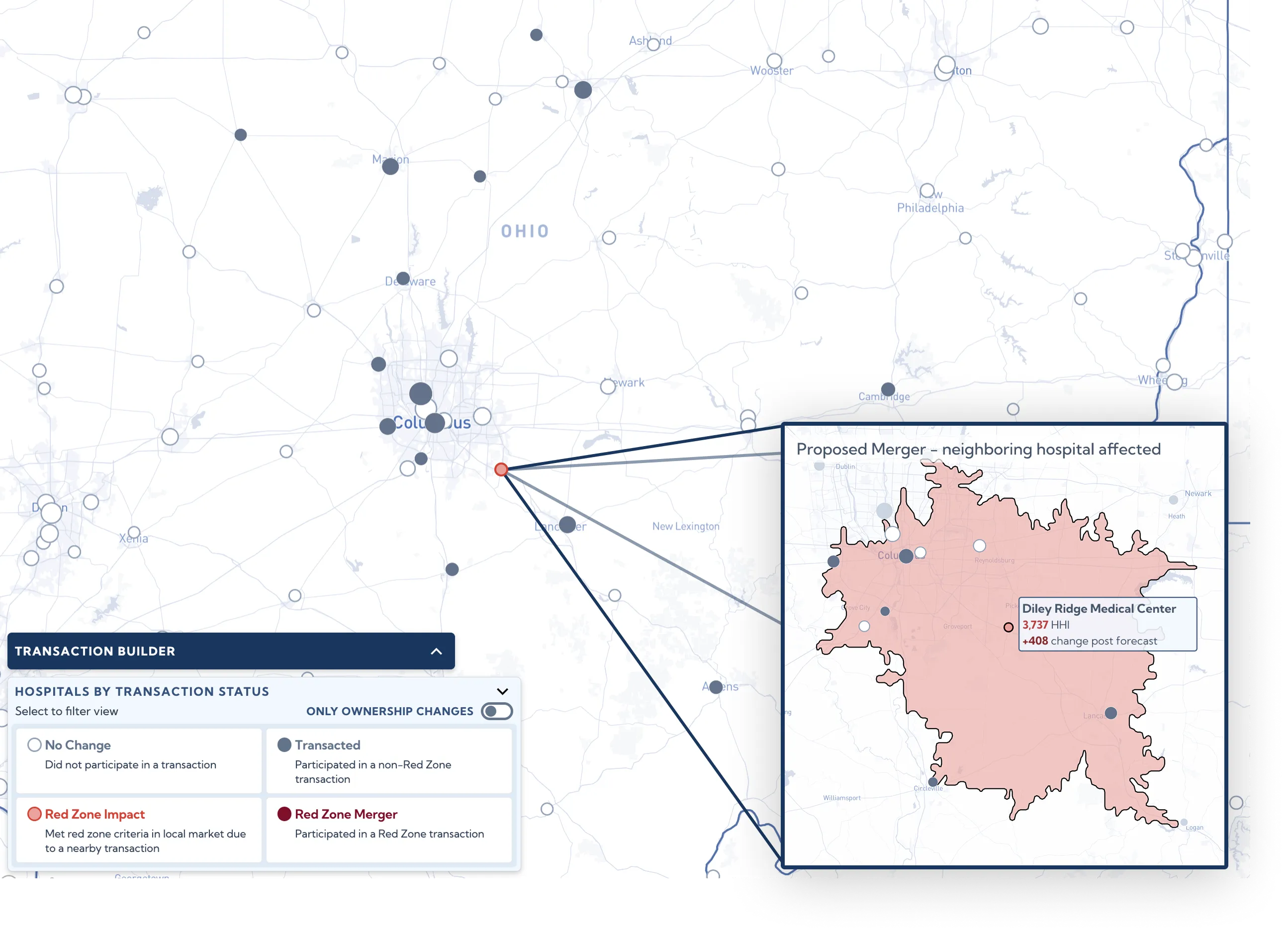

OhioHealth (Columbus, OH) acquiring Fairfield Medical Center (Lancaster, OH).

OhioHealth is seeking to acquire Fairfield Medical Center as its 17th hospital. OhioHealth has acquired 5 hospitals since 2018 and, according to our dataset, operates hospitals in two monopoly markets, six in “higher” concentration markets, and seven “high” concentration markets.

Forecasted Impact: This merger would not affect the market concentration of the hospital or health system involved in the merger, but it would increase the HHI of Diley Ridge Medical Center, which is not involved in the transaction. This is because Diley Ridge Medical Center is geographically close to the merging hospitals.

| Classification | Ripple Effect |

| Combined System Size | 17 hospitals |

| Markets with Increased Concentration | 1 (outside the merger) |

| Largest HHI Increase | +408 (Diley Ridge Medical Center) |

Key Facts:

- This merger would not affect the market concentration for the hospitals directly involved in the merger.

- This merger would increase the concentration of the Diley Ridge Medical Center (Canal Winchester, OH) hospital market by 408 to 3,737 because it is geographically close to both sides of the proposed merger.

- Diley Ridge Medical Center is not affiliated with either health system—it is a nearby facility whose market concentration increases as a ripple effect of the transaction.

Proposed Mergers That Would Reduce Market Concentration

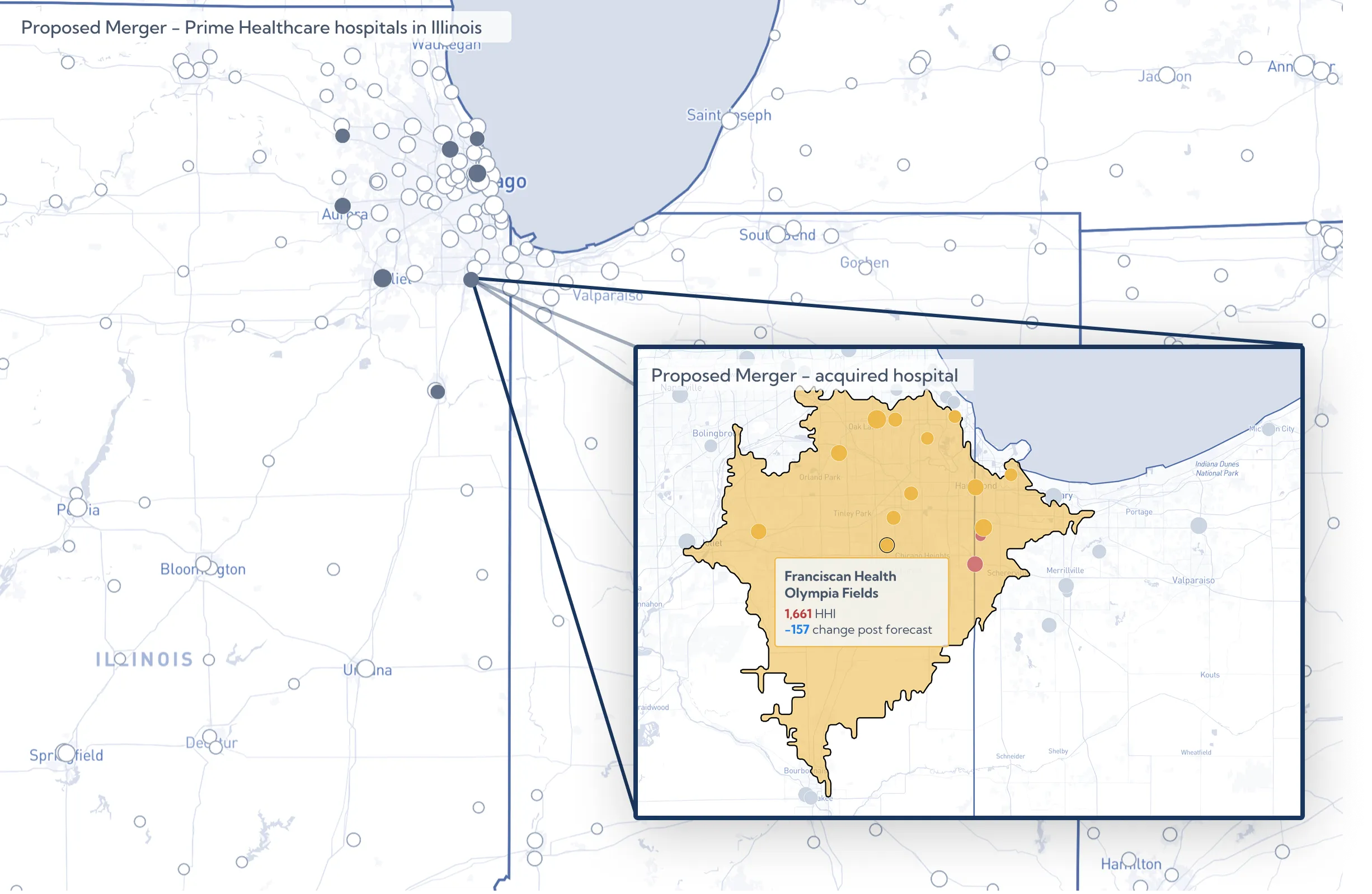

Prime Healthcare (Ontario, CA) acquiring Franciscan Health Olympia Fields (Olympia Fields, IL).

California-based Prime Healthcare (51 hospitals) is seeking to acquire Illinois-based 214-bed Franciscan Health Olympia Fields hospital, currently owned by Franciscan Health, a 13-hospital health system operating in Illinois and Indiana.2

Forecasted Impact: This ownership change would decrease the market concentration of 13 hospitals in Illinois and Indiana, including in Franciscan Health Olympia Fields’ market. A fourteenth hospital not involved in the merger would experience an increase in concentration.

| Classification | Decrease in Concentration |

| Combined System Size | 52 hospitals |

| Markets with Decreased Concentration | 13 (by 11 to 244 points per market) |

| Largest HHI Increase | +208 Silver Cross Hospital (neighbor) |

16 hospitals would be affected by this merger. 13 with decreases to HHI, 1 with an increase of >200, 2 with minor increases.

Key Facts:

- The merger would decrease the HHI of Franciscan Health Olympia Fields’ (St. James Hospitals & Health Centers in the data visualization tool) hospital market by 157 to 1,661.

- The merger would decrease the HHIs for 12 other hospitals (by between 11 and 244 points), three of which are owned by Franciscan Health.

- The merger would newly classify one of the markets for Prime Healthcare’s hospital as highly concentrated. The merger would increase the HHI of Silver Cross Hospital, which is not directly involved in the merger, by 208 to 1,633.

Proposed Mergers That Would Not Impact Market Concentration

MultiCare Health System (Tacoma, WA) acquiring Samaritan Health Services (Corvallis, OR).

Washington-based MultiCare Health System (13 hospitals) is seeking to acquire Oregon-based Samaritan Health Services (5 hospitals) to create an 18-hospital system. The proposed merger is currently under review by the Oregon Health Authority.3

Samaritan Health Services presently operates hospitals in five monopoly markets (HHI of 10,000) in Oregon. MultiCare Health System operates hospitals in six “higher” concentrated markets and five “high” concentrated markets in Washington.

Forecasted Impact: This merger would not have any effect on the HHIs of any hospital markets within the two systems, nor on any markets outside the systems.

| Classification | No HHI Impact |

| Combined System Size | 16 hospitals |

| Markets with Increased Concentration | 0 |

| Note | All 5 of the Samaritan hospitals are considered monopolies (by our definition) |

University of Pittsburgh Medical Center (UPMC) (PA) is acquiring Trinity Health System (OH).

Pennsylvania-based UPMC (35 hospitals) is seeking to acquire Ohio-based Trinity Health System (3 hospitals). Trinity Health System is owned by Chicago-based CommonSpirit Health, which operates approximately 80 hospitals across the U.S.

Forecasted Impact: This merger would not have any effect on the HHIs of any hospital markets within the two systems, nor on any markets outside the systems. This transaction would add one hospital operating in a market that has a “high” concentration and two hospitals operating in markets with “higher” concentrations to the UPMC health system.

| Classification | No HHI Impact |

| Combined System Size | 38 hospitals |

| Markets with Increased Concentration | 0 |

| Note | All 3 of the Trinity hospitals are considered monopolies (by our definition) |

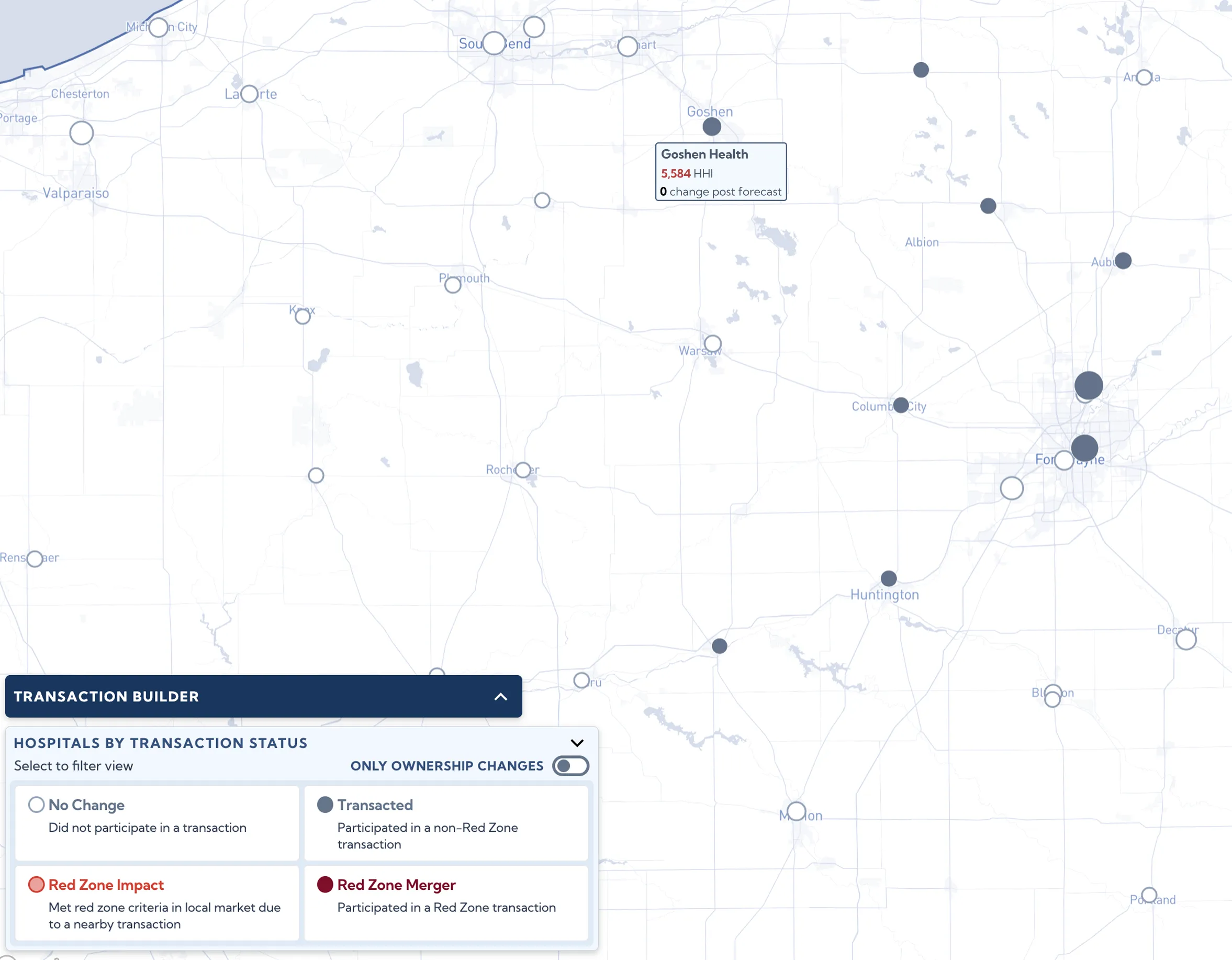

Parkview Health (Fort Wayne, IN) is acquiring Goshen Health (Goshen, IN).

Indiana-based Parkview Health4 (14 hospitals) is seeking to acquire Goshen Health, a 105-bed independently owned hospital. Goshen Health currently operates in a “higher” concentration market.

Forecasted Impact: This merger would have no effect on the market concentration of Goshen Hospital or Parkview Health’s hospitals.

| Classification | No HHI Impact |

| Combined System Size | 9 hospitals |

| Markets with Increased Concentration | 0 |

| Largest HHI Increase | No changes |

.webp)

.webp)

More Commentary

Where America's Hospitals Are Closing — and Opening

Just the Facts on Health Care Consolidation